Has Google recently turned up the visibility dial for “brands”?

Every consulting pitch deck has a “build a strong brand” slide. We all know “brand” is important for SEO.

We’ve all heard Eric Schmidt’s quote: “Brands are the solution, not the problem. Brands are how you sort out the cesspool.”

The impact of branding is not exclusive to SEO. The whole industry of brand marketing exists because consumers seek out brands they trust.

But Schmidt’s quote dropped in 2008 (when users were interestingly just as frustrated with web results as today). Back then, Google didn’t understand content as well as today and leaned much more on user and basic backlink signals.

Today, the organic search landscape looks very different:

- SERP features dominate.

- Shopping results are a marketplace instead of a search engine.

- The recent August 2024 core update looked specifically after independent publishers after a huge wave of outrage when larger brands gained even more visibility in the March 2024 core update.

So, have “brands” gained? The answer is yes, but only in some verticals. But what even defines a brand?

Definition

In the context of SEO, I define a “brand” as a domain that gets:

- Significant brand search volume.

- Higher than expected CTR.

- A knowledge card.

- High brand recall/NPS.

- Growing number of brand keywords.

- A meaningful number of relevant backlinks with brand anchor text.

The way it might materialize in Search:

- Brands see higher than average conversion rates because users trust brands more.

- Users search for brand combination keywords, like “shopify brand name generator”

- It’s likely that brand signals outweigh other signals as big brands get away with more.

Google gives brands preferential treatment because:

- Users want them. Schmidt said in the same interview about the cesspool: “Brand affinity is clearly hard wired. It is so fundamental to human existence that it’s not going away. It must have a genetic component.”

- Aggregators can be intermediaries, which is less helpful for searchers (think meta-search engines).

- Google competes with more aggregators head-on (think Amazon/retailers).

The consequences for SEO Aggregators can be severe.

In David vs. Goliath, I analyzed the top 1,000 winner and loser sites over the last 12 months and found that “bigger sites indeed grow faster than smaller sites, but likely not because they’re big but because they’ve found growth levers they can pull over a long time period.”

Important: “ecommerce retailers and publishers have lost the most,” while brands like Lenovo, Sigma, Coleman, or Hanes gained visibility, as I called out in the follow-up article.

Digging deeper into a set of almost 10,000 keywords I track in the Semrush Enterprise Suite, we can see a shift in some verticals over the last 12 months.

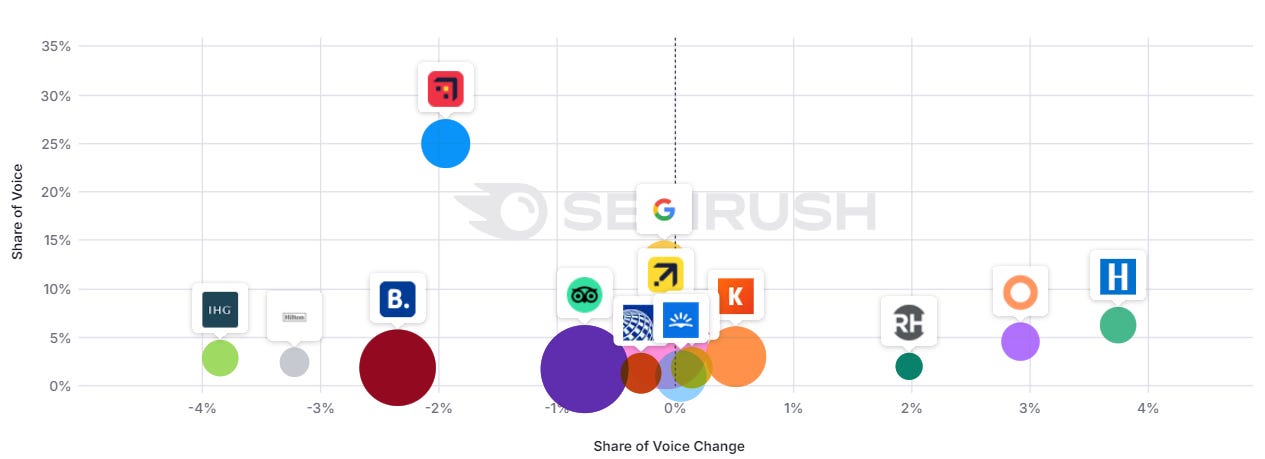

Travel: more brands

Image Credit: Kevin Indig

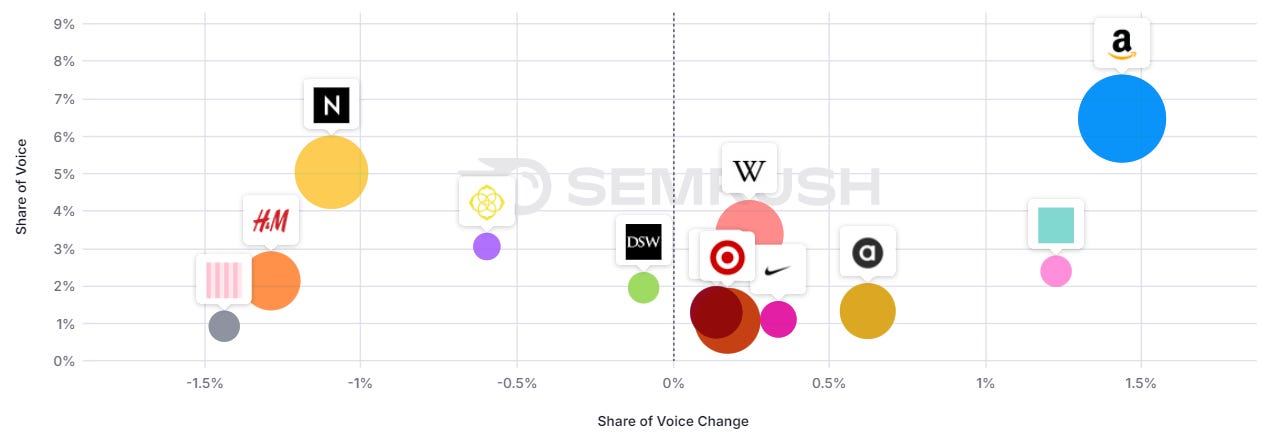

Image Credit: Kevin IndigFashion: mixed picture

Image Credit: Kevin Indig

Image Credit: Kevin IndigBeds: mixed picture

Image Credit: Kevin Indig

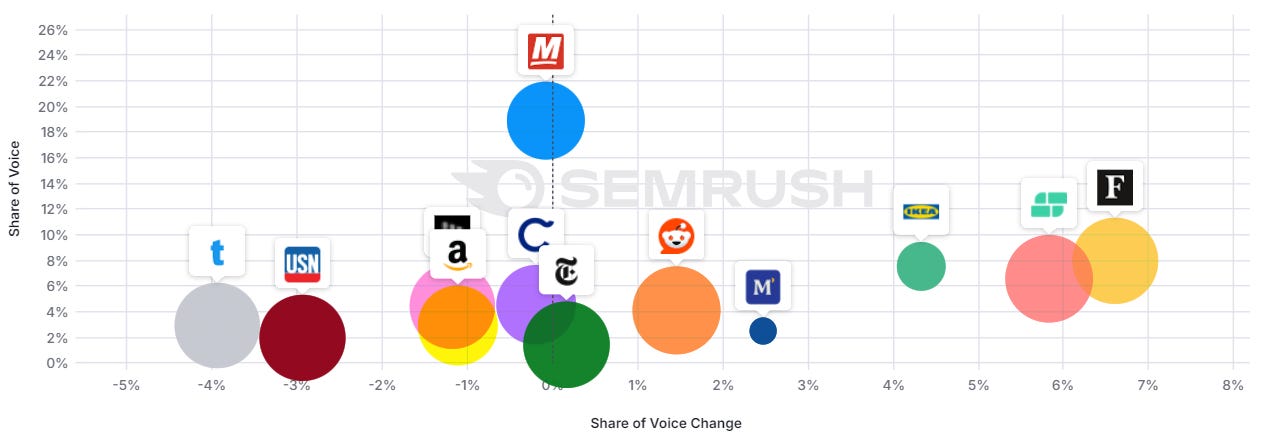

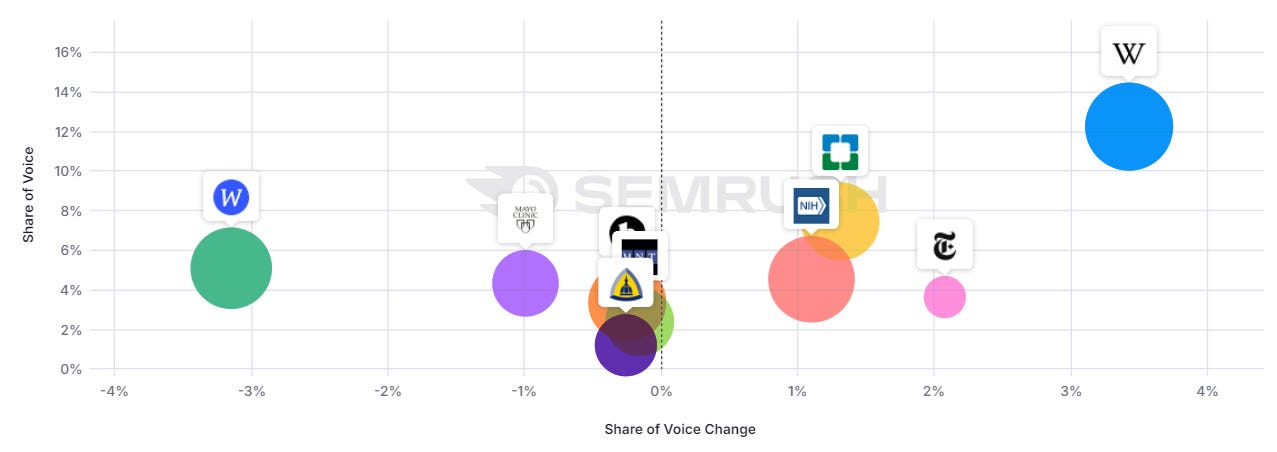

Image Credit: Kevin IndigFinance: more brands

Image Credit: Kevin Indig

Image Credit: Kevin IndigHealth: mixed picture

Image Credit: Kevin Indig

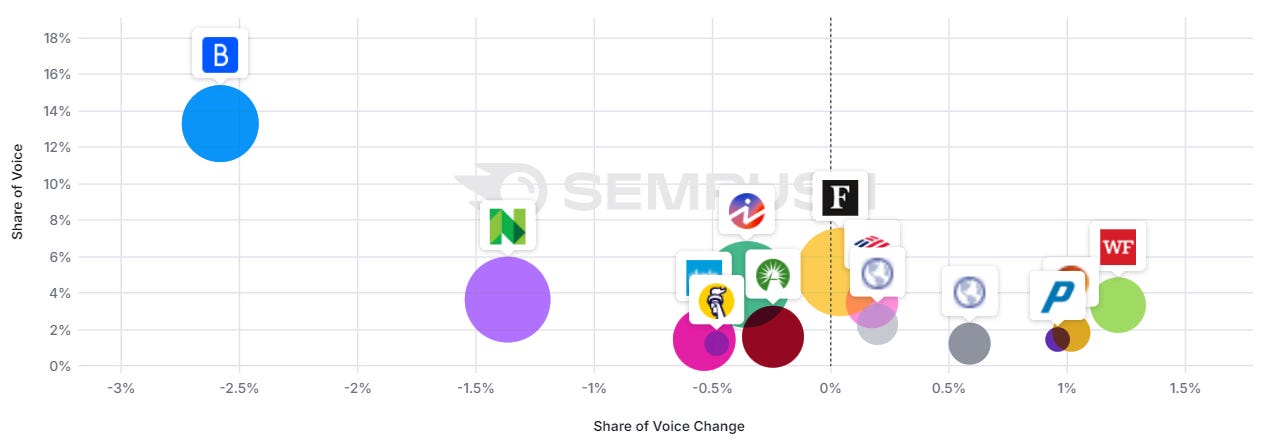

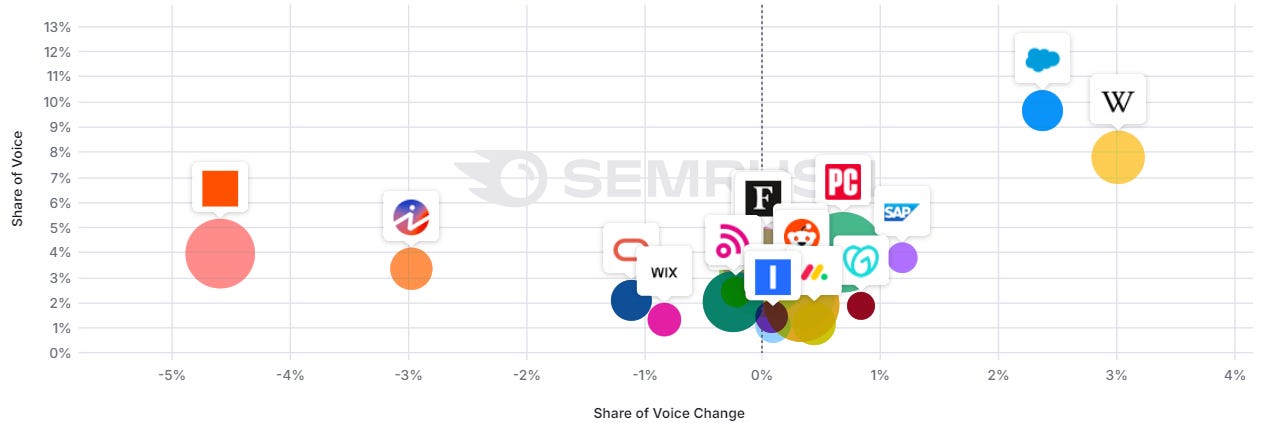

Image Credit: Kevin IndigSaaS: more brands

Image Credit: Kevin Indig

Image Credit: Kevin IndigNote:

- This shift hit not just consumer spaces but B2B as well.

- The impact in ecommerce is harder to judge due to the dominance of free product listings.

- In finance, major players like Nerdwallet lost a lot of visibility (there might be more going on).

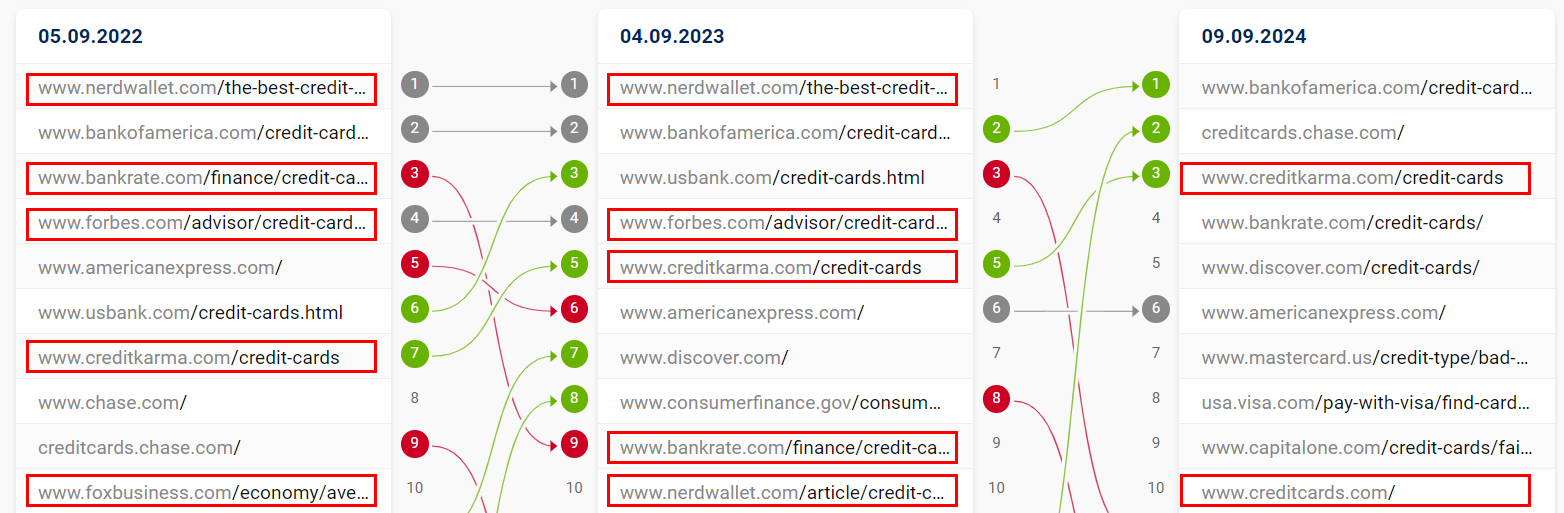

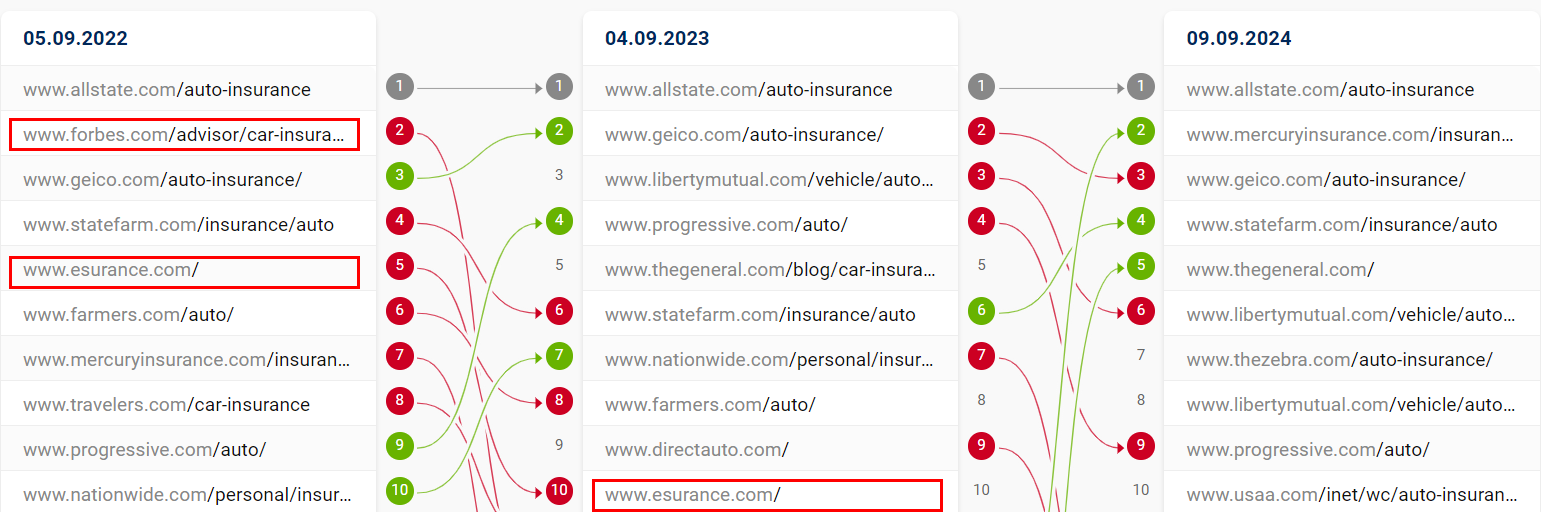

To top it off, three exemplary, hypercompetitive keywords also show major SERP mix shifts over the last two years (non-brands highlighted in red):

Credit Cards: more brands

Image Credit: Kevin Indig

Image Credit: Kevin IndigCar insurance: more brands

Image Credit: Kevin Indig

Image Credit: Kevin IndigWatches: more brands

Image Credit: Kevin Indig

Image Credit: Kevin IndigResponse

Here is how I work with companies that I don’t see as established brands:

We work on reputation by mining reviews on third-party review sites and developing a plan for improving them if necessary.

Google strongly cares about third-party reviews (and so do users), which you can see in the fact that it enriches the shopping graph with them or cites them in the SERPs.

We invest in brand marketing and monitor brand recall/NPS in relation to competitors. We aim always to be a little better, which is part of a larger product strategy.

In my experience, SEO and product are not separable. We monitor and invest in brand mentions and in what context they’re mentioned (co-occurrence).

We consider hard calls when it comes to exact match domains (EMDs). Even though you will find plenty of examples that they work and the cost of migration is very high, sometimes moving to a brand name is the best long-term option. How many EMDs do you know that are memorable?

We take a close look at the ratio of brand to non-brand traffic – are both growing? If you have a low number of branded searches compared to non-branded ones, you don’t have a brand.

We look at brand links and mentions. While generic anchor text links are valuable, people tend to underestimate the impact of brand links on the homepage.

The most effective things you typically do (in the white hat space) for more brand links are also things that get your brand “on the map,” so this also funnels into a larger brand marketing strategy.

Back in 2008, brand links were likely the deciding brand factor.

Today, it’s paired with brand name searches, as Tom Capper’s analysis on Moz shows: domains that lost during Helpful Content Updates had a high ratio of Domain Authority to Brand Authority, meaning lots of links but few brand links.1

Boost your skills with Growth Memo’s weekly expert insights. Subscribe for free!

1 The Helpful Content Update Was Not What You Think

Featured Image: Paulo Bobita/Search Engine Journal